11 Purdeys Way, Rochford, England, SS4 1ND

A pension scheme in the UK is a financial arrangement designed to help individuals save money for their retirement. It’s a structured way to accumulate funds over a person’s working years so that they can support themselves financially when they’re no longer actively working. The UK government and employers often play roles in these schemes.

A pension scheme in the UK is a financial arrangement designed to help individuals save money for their retirement. It’s a structured way to accumulate funds over a person’s working years so that they can support themselves financially when they’re no longer actively working. The UK government and employers often play roles in these schemes.

There are several types of pension schemes in the UK, but the two primary categories are:

Individuals can also set up personal pension plans outside of their workplace, which function similarly to defined contribution workplace schemes. These personal pension plans provide flexibility and allow individuals to choose investment options according to their risk tolerance and retirement goals.

The UK government provides tax incentives to encourage pension saving, such as tax relief on contributions made to pension schemes, which can enhance the growth of the pension fund.

It’s important to plan for retirement by understanding the pension options available, contributing consistently, and making informed decisions about investment choices. The specific details and regulations surrounding pension schemes can vary, so it’s recommended to consult with a financial advisor or visit the official government websites for the most up-to-date and accurate information.

The provision of a workplace pension scheme is of significant importance in ensuring financial security for employees in their retirement years. A workplace pension scheme offers various benefits to employees, such as a way to save for retirement and receive regular income after leaving employment.

By contributing to a pension scheme, employees can accumulate savings over time, which can then be used to fund their retirement. This provides a sense of security, knowing that they will have a stable income during their retirement years.

Additionally, a workplace pension scheme often includes employer contributions, which further enhances the savings potential for employees.

Understanding the auto-enrolment and application process is crucial in order to effectively enroll employees into the pension scheme and ensure their financial security in the future.

An important aspect of the auto-enrolment process is understanding how it works and the steps involved in applying. Employers are required to automatically enroll eligible employees into a workplace pension scheme, ensuring that they can benefit from additional retirement savings.

An important aspect of the auto-enrolment process is understanding how it works and the steps involved in applying. Employers are required to automatically enroll eligible employees into a workplace pension scheme, ensuring that they can benefit from additional retirement savings.

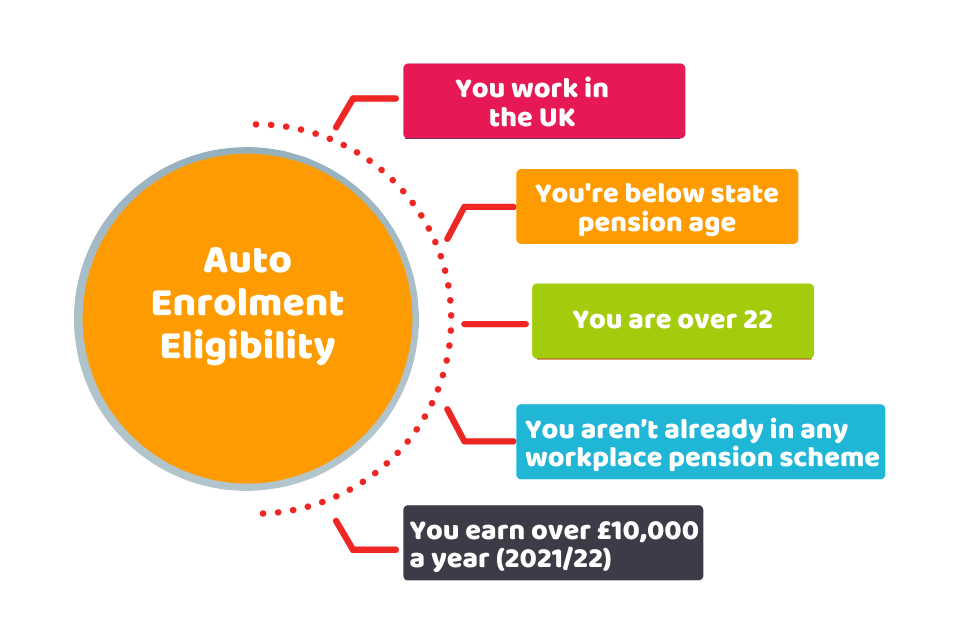

The eligibility criteria for enrolling employees into the scheme include being aged between 22 and the state pension age, earning at least £10,000 per year, and working in the UK. Once employees meet these criteria, they must be enrolled into the pension scheme by the employer.

The application process involves gathering necessary employee information, selecting a pension provider, and making the necessary contributions. Understanding the auto-enrolment process and its application steps is crucial for employers to ensure compliance with pension regulations and provide their employees with access to valuable pension scheme benefits.

Employers and employees are both required to contribute to the pension fund as part of the auto-enrolment process. Contribution limits are set by the government and dictate the maximum amount that can be contributed to a workplace pension scheme. These limits ensure that employees do not exceed tax benefits associated with pension contributions.

Employers must deduct the employee’s contributions from their salary and make additional contributions on their behalf. Employees also benefit from tax relief on their contributions, as these are deducted from their salary before tax is applied. However, employees have the option to opt out of the auto-enrolment process if they do not wish to contribute to the pension fund. This flexibility allows employees to make an informed decision based on their financial circumstances.

Transitioning into the subsequent section on implementing a workplace pension scheme, it is important for employers to understand the requirements and considerations involved in setting up and managing such a scheme.

When implementing a pension plan within a company, it is crucial to carefully consider the legal and regulatory requirements.

Employee benefits, financial planning, and retirement savings are key considerations in the implementation process. Employee benefits play a crucial role in attracting and retaining talent, and a workplace pension scheme can be a valuable offering. It provides employees with a means to save for their retirement and ensures financial security in their post-work years.

Additionally, a well-structured pension scheme can assist employees in their overall financial planning by providing a dedicated savings vehicle. From a regulatory standpoint, employers must ensure compliance with relevant legislation, such as auto-enrollment requirements and contribution limits.

Different types of retirement savings plans should be carefully considered by employers to ensure that the chosen scheme aligns with the specific needs and goals of both the organization and its employees.

Three common types of pension schemes for employers are defined benefit pensions (DB), group personal pensions (GPP), and self-invested personal pensions (SIPP).

Defined benefit pensions guarantee a specific retirement income based on factors such as salary and years of service.

Group personal pensions are provided by employers but managed by external pension providers, offering employees a range of investment options.

Self-invested personal pensions allow individuals to have greater control over their pension investments, with a wider choice of investment options.

Employers should evaluate the advantages and disadvantages of each scheme to determine which one most suitable suits their organization and employees’ needs.

In conclusion, providing a workplace pension scheme is of utmost importance for employers. Understanding the auto-enrolment process and application requirements is crucial.

Both employer and employee contributions play a significant role in ensuring the success of the scheme. Implementing a workplace pension scheme requires careful planning and consideration.

Exploring different types of pension schemes allows employers to choose the most suitable option for their company. Overall, offering a workplace pension scheme demonstrates a commitment to employee financial well-being and can contribute to a positive work environment.

NOTE:

My Key Finance does not provide advice or guidance on pensions and we suggest you speak to a qualified IFA if this is something you would like to discuss.